The chairman of the World Holocaust Remembrance Center has accused Elon Musk of insulting victims of Nazism after the billionaire told a German far-right political party that the country needed to “move beyond” the “guilt” of the past.

Musk made the comments in a surprise video address at an election campaign launch for the far-right Alternative for Germany (AfD) on Saturday.

“Children should not be guilty of the sins of their parents, let alone their great grandparents,” he said.

“There is too much focus on past guilt, and we need to move beyond that,” he added.

Musk’s remarks mirrored the AfD’s long-held position that Germany should stop atoning for crimes committed by the Nazis in the past.

Dani Dayan, the chairman of Yad Vashem, the World Holocaust Remembrance Center, warned against any move to bury the legacy of Nazism. Writing in a post on X, which is owned by Musk, Dayan said that “the remembrance and acknowledgement of the dark past of the country and its people should be central in shaping the German society,” and that “failing to do so is an insult to the victims of Nazism and a clear danger to the democratic future of Germany.”

Musk has taken an increasing interest in European politics and several leaders on the continent have accused him of interfering in their affairs and promoting dangerous figures.

Poland’s Prime Minister Donald Tusk condemned Musk’s comments as “ominous” and “all too familiar,” noting that they came “only hours before the anniversary of the liberation of Auschwitz.”

In his Saturday address, Musk said it was important “that people take pride in Germany and being German,” a remark that was met with rapturous cheers.

Musk also addressed the issue of immigration – a key issue in Germany’s upcoming general election on February 23 – urging AfD co-leader Alice Weidel and her supporters not to lose their national pride in “some kind of multiculturalism that dilutes everything.”

It is not the first time in recent days that Musk has drawn scrutiny for his apparent support for the far-right. Last week, Musk faced a backlash after he made a gesture at a post-inauguration rally last week that some commentators said resembled a fascist salute.

At a rally following US President Donald Trump’s inauguration last Monday, Musk brought his right arm towards his chest and then extended it towards the audience, drawing scrutiny as the gesture bears similarities to the Nazi or Roman salute used by fascist leaders in Germany and Italy.

Musk pushed back on the criticism, writing on X, “the ‘everyone is Hitler’ attack is sooo tired.”

German chancellor Olaf Scholz – a frequent target of Musk’s barbs – told a panel at the World Economic Forum in Davos, Switzerland: “Everyone is free to express their opinion in Germany and Europe, including billionaires… but we do not accept support for far-right positions.” Musk responded on X: “Shame on Oaf Schitz!”

Israeli Prime Minister Benjamin Netanyahu defended Musk, saying that he was “falsely smeared” amid a storm of international condemnation.

The Anti-Defamation League (ADL) initially dismissed it as “an awkward gesture in a moment of enthusiasm.”

However, in response to Musk posting a series of Nazi puns to social media on Thursday, the ADL hit out at “inappropriate and highly offensive jokes that trivialize the Holocaust.”

Despite the scrutiny, Musk has continued to voice his support for populist political movements that have galvanized numerous European elections. He has also drawn parallels between the political climate in Germany and the United States while emphasizing the global impact the approaching election could have.

Violent weather exacerbated by climate change fueled hunger and food insecurity across Latin America and the Caribbean in 2023, according to a new United Nations report.

Extreme weather drove up crop prices in multiple countries in the region in 2023, the report, which was written by several UN agencies including the World Food Program (WFP), says.

Hot weather and drought, intensified by the El Niño weather phenomenon, raised the price of corn in Argentina, Mexico, Nicaragua and the Dominican Republic, while heavy rain in Ecuador caused a 32 to 54 percent increase in wholesale prices in the same year.

Though the report credits social safety nets with a measurable decrease in undernourishment throughout Latin America, it notes that the region’s poorest and most vulnerable populations are still more likely to suffer from food insecurity due to climate change – especially rural people.

Quoting a 2020 study, the report states that 36% of 439 small farms surveyed in rural Honduras and Guatemala experienced “episodic food insecurity due to extreme weather events.”

“In more rural areas they…don’t have a lot of resources to be able to weather a poor harvest,” said Ivy Blackmore, a researcher affiliated with the University of Missouri who studied nutrition and agriculture among Indigenous farming communities in Ecuador.

“You don’t generate as much income. There’s not as much nutritious food around, so they sell what they can, and then they purchase the cheapest thing that’ll fill them up,” she added.

In the communities she studied, erosion from prolonged rain led farmers to plant on virgin grassland nearby.

“They might have a couple of good harvests. Then the erosion continues, and they dig up more,” Blackmore said. “There’s extreme erosion going on because they’re just having to sustain themselves in the short term without being able to address these long-term consequences.”

As extreme weather increases food prices, some consumers gravitate toward cheaper, but less nutritious, ultra-processed foods. This is a particularly dangerous trend in Latin America, the UN report says, where “the cost of healthy diets is the highest in the world” and both childhood and adult obesity have risen markedly since 2000.

NorthStar Gaming Holdings Inc. (TSXV: BET) (OTCQB: NSBBF) (‘NorthStar’ or the ‘Company’) is pleased to announce the Company has, subject to final approval of the TSX Venture Exchange, entered into a credit agreement (the ‘Credit Agreement’) in respect of a senior secured first lien term loan facility providing for loans in an aggregate principal amount of up to $43.4 million CAD (being the approximate equivalent of $30,000,000 USD) (the ‘Credit Facility’) to be made available by Beach Point Capital Management LP (‘Beach Point’). Playtech plc (‘Playtech’) and certain Playtech subsidiaries have agreed to provide credit support for certain obligations under the Credit Facility. The Credit Facility represents a significant milestone for NorthStar, strengthening its balance sheet and enabling the Company to continue to accelerate its growth initiatives.

Executive Commentary

‘This is a pivotal moment for NorthStar, marking the largest financing in our history. This Credit Facility strengthens our balance sheet and directly supports our ability to scale operations and drive the business towards profitability with a single-minded focus,’ said Michael Moskowitz, Chair and CEO of NorthStar. ‘We are grateful to Beach Point Capital Management for their trust in our strategy and vision. We are also thankful for Playtech’s steadfast partnership which was instrumental in securing this funding, reinforcing their value both strategically and as a technology provider.’

‘Beach Point has deep experience investing across the gaming sector and is excited to partner with NorthStar to support their strategic initiatives. The online gaming sector has been growing rapidly, and this investment reflects our confidence in the Company’s leadership, market potential, and ability to deliver long-term sustainable growth. Likewise, we value the partnership with Playtech, who are contributing their leading technology, global reach, and strategic vision towards NorthStar’s continued success,’ said Gabriel Fineberg, Managing Director at Beach Point.

Purpose of the Credit Facility

The purpose of the Credit Facility is to support NorthStar’s continued growth by significantly strengthening the Company’s balance sheet. The Company will use the proceeds of loans made pursuant to the Credit Facility: (i) to repay the aggregate $9.5 million CAD principal amount (plus accrued interest) loaned to the Company by Playtech pursuant to unsecured, interest-bearing promissory notes dated April 25, 2024, September 13, 2024 and December 16, 2024; (ii) to fund an interest reserve account in respect of the Credit Facility in an amount equal to $7,000,000 CAD; (iii) for working capital and general corporate purposes; and (iv) to pay transaction costs in connection with the Credit Facility.

Key Terms of the Credit Facility

Loan Amount: $43.4 million CAD

Interest Rate: SOFR + 9.35%, with a SOFR floor of 4.40%

Maturity Date: January 24, 2030

Amortization: Payment deferral for the first 30 months, followed by 2.5% per annum of the principal amount until the 42nd month ending after the closing date (paid quarterly), and, thereafter, 5% per annum until the Maturity Date (paid quarterly).

The Credit Facility is secured by a first-priority lien on substantially all of the assets of NorthStar and its wholly-owned subsidiaries (the ‘NorthStar Guarantors’). The NorthStar Guarantors have provided a guarantee of the obligations of the Company under the Credit Agreement and the other loan documents.

A copy of the Credit Agreement will be available on NorthStar’s SEDAR+ profile at www.sedarplus.ca.

Credit Support from Playtech

In addition to the guarantee by the NorthStar Guarantors, it is also a requirement of the Credit Agreement that Playtech, together with certain of its affiliates (the ‘Playtech Guarantors’) guarantee the obligations of the Company under the Credit Agreement and the other loan documents (the ‘Playtech Guarantee’). In consideration of the Playtech Guarantors providing the Playtech Guarantee, and subject to receipt of all required regulatory approvals (including final approval of the TSX Venture Exchange), NorthStar has issued to Playtech 32,735,295 common share purchase warrants (‘Bonus Warrants’), exercisable at a price of $0.055 CAD per share, reflecting an approximately 8.70% premium to the five-day volume-weighted average price of the common shares of the Company on January 24, 2025. The Bonus Warrants will be subject to a trading hold period expiring four months from the date of issue under applicable securities laws. The Bonus Warrants expire on January 24, 2030 and are non-transferable. In accordance with the policies of the TSX Venture Exchange, if at any time the outstanding principal amount under the Credit Facility is reduced or repaid during the first year of the term of the Credit Facility, the expiry date in respect of a pro rata number of the total Bonus Warrants will be accelerated to the later of: (a) one year from the date of issuance of the Bonus Warrants; and (b) 30 days from such reduction or repayment of the Credit Facility.

Playtech is an insider of the Company and the issuance of the Bonus Warrants in connection with the provision of the Playtech Guarantee will be considered a ‘related party transaction’ under Multilateral Instrument 61-101 – Protection of Minority Security Holders in Special Transactions (‘MI 61-101’). The Company intends to rely on the exemptions set forth in sections 5.5(b) and 5.7(a) of MI 61-101 from the valuation and minority shareholder approval requirements of MI 61-101 in respect of the issuance of the Bonus Warrants in connection with the provision of the Playtech Guarantee, as the Company is not listed on one of the specified markets in section 5.5(b) of MI 61-101 and the aggregate fair market value of the Bonus Warrants will be less than 25% of the Company’s market capitalization.

A material change report in respect of, inter alia, the issuance of the Bonus Warrants to Playtech in connection with the provision of the Playtech Guarantee will be filed in accordance with MI 61-101. Such material change report was not filed at least 21 days before the issuance of the Bonus Warrants to Playtech in connection with the provision of the Playtech Guarantee as the Company wanted to close and implement these arrangements on an expedited basis for sound business reasons.

Advisors

NorthStar would like to express its gratitude to the advisory teams that facilitated this successful transaction. The Company was co-advised by XST Capital Group LLC and Roselli Advisory LLC, who provided financial advisory services to NorthStar, and Norton Rose Fulbright Canada LLP, who acted as legal counsel to NorthStar.

Kirkland & Ellis LLP and Goodmans LLP acted as legal counsels to Beach Point.

About NorthStar

NorthStar proudly owns and operates NorthStar Bets, a Canadian-born casino and sportsbook platform that delivers a premium, distinctly local gaming experience. Designed with high-stakes players in mind, NorthStar Bets Casino offers a curated selection of the most popular games, ensuring an elevated user experience. Our sportsbook stands out with its exclusive Sports Insights feature, seamlessly integrating betting guidance, stats, and scores, all tailored to meet the expectations of a premium audience.

As a Canadian company, NorthStar is uniquely positioned to cater to customers who seek a high-quality product and an exceptional level of personalized service, setting a new standard in the industry. NorthStar is committed to operating at the highest level of responsible gaming standards.

NorthStar is listed in Canada on the Toronto Stock Venture Exchange under the symbol BET and in the United States on the OTCQB under the symbol NSBBF. For more information on the company, please visit: www.northstargaming.ca

About Beach Point

Beach Point is a multi-strategy investment manager making credit, private equity, real estate and structured product investments. As of December 31, 2024, Beach Point manages approximately $19 billion in AUM on behalf of a predominantly institutional client base. Headquartered in Santa Monica, CA, Beach Point also has offices in New York, London and Dublin. For more information, visit https://beachpoint.capital.

No stock exchange, securities commission or other regulatory authority has approved or disapproved the information contained herein. Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this press release.

Cautionary Note Regarding Forward-Looking Information and Statements

This communication contains ‘forward-looking information’ within the meaning of applicable securities laws in Canada (‘forward-looking statements’), including without limitation, statements with respect to the following: the expected benefits of the Credit Facility, the use of proceeds of the Credit Facility, the ability of the Company to perform its obligations under the Credit Facility, and future value to be delivered as a result of the Credit Facility and the Company’s ability to continue as a going concern (whether or not the Credit Facility is available in the short- and long-term). The foregoing is provided for the purpose of presenting information about management’s current expectations and plans relating to the future and allowing investors and others to get a better understanding of the Company’s anticipated financial position, results of operations, and operating environment. Often, but not always, forward-looking statements can be identified by the use of words such as ‘plans’, ‘expects’, ‘is expected’, ‘budget’, ‘scheduled’, ‘estimates’, ‘continues’, ‘forecasts’, ‘projects’, ‘predicts’, ‘intends’, ‘anticipates’ or ‘believes’, or variations of, or the negatives of, such words and phrases, or state that certain actions, events or results ‘may’, ‘could’, ‘would’, ‘should’, ‘might’ or ‘will’ be taken, occur or be achieved. This information involves known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking statements. This forward-looking information is based on management’s opinions, estimates and assumptions that, while considered by NorthStar to be appropriate and reasonable as of the date of this press release, are subject to known and unknown risks, uncertainties, assumptions and other factors that may cause the actual results, levels of activity, performance, or achievements to be materially different from those expressed or implied by such forward- looking information. Such factors include, among others, the following: risks related to the Company’s business and financial position; risks associated with general economic conditions; adverse industry risks; future legislative and regulatory developments; the ability of the Company to implement its business strategies; and those factors discussed in greater detail under the ‘Risk Factors’ section of the Company’s most recent annual information form, which is available under NorthStar’s profile on SEDAR+ at www.sedarplus.com. Many of these risks are beyond the Company’s control.

If any of these risks or uncertainties materialize, or if the opinions, estimates or assumptions underlying the forward-looking information prove incorrect, actual results or future events might vary materially from those anticipated in the forward-looking statements. Although the Company has attempted to identify important risk factors that could cause actual results to differ materially from those contained in the forward-looking statements, there may be other risk factors not presently known to the Company or that the Company presently believes are not material that could also cause actual results or future events to differ materially from those expressed in such forward-looking statements. There can be no assurance that such information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. No forward-looking statement is a guarantee of future results. Accordingly, you should not place undue reliance on forward-looking information, which speaks only as of the date made. The forward-looking information contained in this press release represents NorthStar’s expectations as of the date specified herein, and are subject to change after such date. However, the Company disclaims any intention or obligation or undertaking to update or revise any forward-looking information whether as a result of new information, future events or otherwise, except as required under applicable securities laws.

All of the forward-looking information contained in this press release is expressly qualified by the foregoing cautionary statements.

For further information:

Company Contact:

Corey Goodman Chief Development Officer 647-530-2387 investorrelations@northstargaming.ca www.northstargaming.ca

Investor Relations:

RB Milestone Group LLC (RBMG) northstar@rbmilestone.com

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/238526

NOT FOR DISTRIBUTION TO U.S. NEWSWIRE SERVICES OR FOR RELEASE, PUBLICATION, DISTRIBUTION OR DISSEMINATION, DIRECTLY OR INDIRECTLY, IN WHOLE OR IN PART, IN OR INTO THE UNITED STATES.

January 27, 2025 TheNewswire – Vancouver, British Columbia, Canada JZR Gold Inc. (TSXV: JZR) (OTCQB: JZRIF) (the ‘ Company ‘ or ‘ JZR ‘) wishes to provide an update on operations at Vila Nova gold project (the ‘ Vila Nova Project ‘) located in the state of Amapa, Brazil. The Company possesses a 50% net profit interest in all net profit generated from the Vila Nova Project pursuant to a Joint Venture Royalty Agreement dated July 6, 2020, as amended on January 9, 2023, with ECO Mining Oil & Gaz Drilling Exploration EIRELI (‘ ECO ‘). ECO, as the operator of the Vila Nova Project, has commissioned the manufacture of an 800 tonne-per-day gravimetric mill, which mill (the ‘ Mill ‘) has been assembled and is located on the Vila Nova property. ECO has advised the Company that the Mill has been energized and that it is currently testing each individual component, including pumps and hoses. ECO has indicated to the Company that it expects that the Mill will commence operating as soon as practicable after testing has been completed.

The Company also announces that it intends to undertake a non-brokered private placement offering (the ‘ Offering ‘) of up to 2,400,000 units (each, a ‘ Unit ‘) at a price of $0.25 per Unit, to raise aggregate gross proceeds of up to $600,000. Each Unit will be comprised of one common share (each, a ‘ Share ‘) and one share purchase warrant (each, a ‘ Warrant ‘). Each Warrant will entitle the holder to acquire one additional common share (each, a ‘ Warrant Share ‘) of the Company at an exercise price of $0.35 per Warrant Share for a period of three (3) years after the closing of the Offering. The Warrants will be subject to an acceleration provision whereby, in the event that the volume weighted average trading price of the Company’s common shares traded on TSX Venture Exchange (the ‘ Exchange ‘), or any other stock exchange on which the Company’s common shares are then listed, is equal to or greater than $0.75 for a period of 10 consecutive trading dates, the Company shall have the right to accelerate the expiry date of the Warrants by giving written notice to the holders of the Warrants that the Warrants will expire on the date that is not less than 30 days from the date that notice is provided by the Company to the Warrant holders.

The Company intends to pay registered persons a finder’s fee comprised of 6% of the gross proceeds of the Offering, in cash, and such number of non-transferable finder’s warrants which equals 6% of the number of Units (the ‘ Finder’s Warrants ‘). Each Finder’s Warrant shall entitle the holder to acquire one common share (the ‘ Finder’s Warrant Shares ‘) at a price of $0.35 per Finder’s Warrant Share for a period of three (3) years from the date of issuance. Other than being non-transferable, each Finder’s Warrant shall otherwise be on the same terms as the Warrants. The Units, Shares, Warrants, Warrant Shares, Finder’s Warrants and Finder’s Warrant Shares are collectively referred to herein as the ‘ Securities ‘.

The Units will be offered pursuant to available prospectus exemptions set out under applicable securities laws and instruments, including National Instrument 45-106 – Prospectus Exemptions.

It is expected that certain Insiders (as such term is defined under the policies of the Exchange) of the Company may participate in the Offering. The participation of Insiders in the Offering will constitute a ‘related party transaction’ within the meaning of Multilateral Instrument 61-101 – Protection of Minority Security Holders in Special Transactions (‘ MI 61-101 ‘). The Company intends to rely on exemptions from the formal valuation and minority shareholder approval requirements provided under subsections 5.5(a) and 5.7(a) of MI 61-101 on the basis that participation in the Offering by Insiders will not exceed 25% of the fair market value of the Company’s market capitalization.

The Offering may close in one or more tranches, as subscriptions are received. The Securities will be subject to a hold period of four months and one day from the date of issuance. Closing of the Offering, which is expected to occur on or about February 7, 2025, will be subject to satisfaction of certain conditions, including, but not limited to, the receipt of all necessary regulatory and other approvals, including approval by the Exchange.

The Company intends to use the net proceeds from the Offering to fund operations of the Mill as well as future exploration work on the Vila Nova Project, all by way of one or more loans to ECO, and for general working capital purposes.

For further information, please contact:

Robert Klenk

Chief Executive Officer

rob@jazzresources.ca

Forward-Looking Information

This press release contains certain ‘forward-looking information’ within the meaning of applicable Canadian securities legislation. Forward-looking information in this press release includes all statements that are not historical facts, including, without limitation, statements with respect to the details of the Offering, including the proposed size, timing and the expected use of proceeds and the receipt of regulatory approval for the Offering; the testing and anticipated commencement of operation of the Mill. Forward-looking information reflects the expectations or beliefs of management of the Company based on information currently available to it. Forward-looking information is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed or implied by such forward-looking information. These factors include, but are not limited to: the Company may not complete the Offering; the Offering may not be approved by the TSX Venture Exchange; risks associated with the business of the Company; the Mill may not commence operating once testing has been completed, or at all; business and economic conditions in the mineral exploration industry generally; the supply and demand for labour and other project inputs; changes in commodity prices; changes in interest and currency exchange rates; risks related to inaccurate geological and engineering assumptions; risks relating to unanticipated operational difficulties (including failure of equipment or processes to operate in accordance with the specifications or expectations, cost escalation, unavailability of materials and equipment, government action or delays in the receipt of government approvals, industrial disturbances or other job action and unanticipated events related to health, safety and environmental matters); risks related to adverse weather conditions; political risk and social unrest; changes in general economic conditions or conditions in the financial markets; and other risk factors as detailed from time to time in the Company’s continuous disclosure documents filed with the Canadian securities regulators. The forward-looking information contained in this press release is expressly qualified in its entirety by this cautionary statement. The Company does not undertake to update any forward-looking information, except as required by applicable securities laws.

Neither the TSX Venture Exchange nor its regulation services provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this press release.

None of the securities of JZR have been registered under the U.S. Securities Act of 1933, as amended (the ‘U.S. Securities Act’), or any state securities law, and may not be offered or sold in the United States or to, or for the account or benefit of, persons in the United States or ‘U.S. persons’ (as such term is defined in Regulation S under the U.S. Securities Act) absent registration or an exemption from such registration requirements. This press release shall not constitute an offer to sell or the solicitation of an offer to buy in the United States nor shall there be any sale of the securities in any State in which such offer, solicitation or sale would be unlawful.

Copyright (c) 2025 TheNewswire – All rights reserved.

Female Republicans in Congress are fighting to change the decadeslong narrative that paints Democrats as the party of women, hoping it transcends to significant gains in future elections.

‘We’ve got to get back to our roots of being the party of women,’ Rep. Nicole Malliotakis, R-N.Y., told Fox News Digital. ‘I don’t know why we ever allowed the Democrats to hijack the narrative and claim to be the party of women. That’s bull.’

Other GOP lawmakers who spoke with Fox News Digital about this story noted that cost of living, a cornerstone issue for Republicans in the last election, was as much a women’s issue as anyone else’s.

Republicans have also passed several bills since winning that election that have put women at the focus of conservative policy changes on transgender youth and border security.

‘You should not let the Democrat Party tell you they’re the party of women if they can’t even define what a woman is. So we are going to continue to be strong advocates for young women and girls, whether that’s in professional spaces, in bathrooms or in sports,’ said Rep. Ashley Hinson, R-Iowa, referencing a recently passed bill keeping biological male student athletes out of girls’ sports teams and locker rooms.

Hinson said she is ‘a working mom fighting for other working moms.’

‘Women are oftentimes the most important decision makers in a household, for example. So, when I’m thinking about economic indicators, how are we going to get more women in the workforce? How can we empower more women and families? How can we support more women in sports?’ Hinson posed.

Historically, Malliotakis pointed out, it was Republicans who led passage of the 19th Amendment that secured women the right to vote. She also pointed out that it was under President Donald Trump that a museum dedicated to women’s history was authorized.

‘President Trump authorized in 2020 the Smithsonian Women’s History Museum. And Joe Biden did nothing with it for four years,’ Malliotakis said. ‘ ‘I’ve been pushing a land transfer for the Smithsonian women’s museum to be built, and I think it makes total sense that we would be the party that would do this, considering our history.’

As a voting bloc, women have favored Democrats and the left in recent history.

Democrats have also blamed Republicans for the conservative-leaning Supreme Court overturning Roe v. Wade, a move that did appear to translate to electoral success in the 2022 midterms.

Progressives were also historically the biggest supporters of the Equal Rights Amendment, legislation that was pushed primarily during the second-wave feminist movement.

However, Republican women like Rep. Nancy Mace, R-S.C., are now arguing that bills like hers, which would deport illegal immigrants who commit sex crimes against women and other Americans, are what it takes to protect women.

‘MAGA is the new feminist,’ Mace wrote on X this month.

Additionally, Rep. Julie Fedorchak, R-N.D., one of the few Republican women in the 119th Congress’ freshmen class, pointed out that her own story was a testament to GOP meritocracy.

‘I was the largest vote-getter in my whole state out of anybody, as a woman, as the first congresswoman in our state. So I think more than anything else, people want folks who are primed for the job, who are competent and ready,’ Fedorchak said.

‘The cost of everything, making ends meet, helping women manage their multiple roles, getting government out of their lives, helping reinforce the role of parents…these are things that are women’s issues.’

Sen. Mike Lee is continuing to call for the abolition of the Transportation Security Administration (TSA).

‘Tired of being groped every time you travel? Abolish TSA,’ the senator said in a recent post on X.

‘Make Airport Security Free Of Sexual Assault Again,’ Lee said in another tweet, adding, ‘Abolish TSA.’

In another post, he suggested that President Donald Trump should eliminate the TSA.

Lee suggests that instead of TSA, airlines could handle passenger screening.

‘You may be required to undergo a pat-down procedure if the screening technology alarms, as part of unpredictable security measures, for enhanced screening, or as an alternative to other types of screening, such as advanced imaging technology screening,’ according to the TSA website. ‘A pat-down may include inspection of the head, neck, arms, torso, legs, and feet. This includes head coverings and sensitive areas such as breasts, groin, and the buttocks.’

The agency was established in the wake of the Sept. 11, 2001, terror attacks.

‘The Aviation and Transportation Security Act, passed by the 107th Congress and signed on November 19, 2001, established TSA,’ according to the TSA’s website.

Lee advocated the idea of nixing TSA last year as well.

‘It’s time to abolish the TSA. Airlines can and will secure their own planes if a federal agency doesn’t do it for them. They’ll do it better than TSA, without undermining the Constitution and with less groping—showing more respect for passengers,’ the senator declared in a post last year on March 11.

Days later, Lee indicated that he had been subjected to a TSA pat down.

‘Update: days after calling to abolish TSA, I got ‘randomly selected’ for the needlessly slow, thorough TSA screening & patdown. Maybe it’s a coincidence. Or not. Impossible to know. That’s part of the problem with having a federal agency in charge of airport security,’ he tweeted on March 14, 2024.

In December, the senator shared a video of a man being subjected to a pat down.

‘It’s unsettling knowing that the TSA does this countless times every day, constantly conducting needlessly invasive, warrantless, suspicion-less searches of law-abiding Americans,’ Lee wrote when sharing the video. ‘Please share if you’d like to abolish TSA,’ he added.

“It doesn’t do any good for your heart, for your mind, for anything,” said Holocaust survivor Jona Laks, 94, about her return to Nazi Germany’s Auschwitz-Birkenau concentration camp.

“But it’s necessary,” she said. “It’s necessary for the world to know.”

Monday marks Holocaust Memorial Day and the 80th anniversary of the liberation of the Auschwitz camp complex, where Laks spent more than a year when she was only about 12 years old.

She and her twin sister, Miriam, experienced horrors in the inhumane medical experiments of SS physician Josef Mengele. Laks was initially lined up to be murdered in gas chambers, but her older sister saved her by shouting that the twins should not be separated.

“As time passes over, things are being forgotten,” Laks said, noting that few are left from her generation to speak out. “The world hasn’t learned its lessons from what happened, from what was done.”

Approximately 1.1 million people were murdered at the concentration camp from 1940 to 1945, many of them Jews but also other victims of the Third Reich including Poles, the Roma, and Soviet prisoners of war.

Michael Bornstein, who survived for seven months inside Auschwitz as a child, said that “nothing will be easy about returning” to the site.

World leaders are also gathered in Poland to mark the camp’s liberation, including Britain’s King Charles, German Chancellor Olaf Scholz and French President Emmanuel Macron. But none will speak at the event, which instead aims to focus on the voices of survivors.

All of Auschwitz’s remainingsurvivors are invited to the commemorations and can bring one person for support.

“We are fully aware of how physically demanding and emotionally taxing attending the commemoration event at the site of the former camp can be for them,” the Auschwitz Memorial and Museum said in a statement.

One of the symbols of the 80th anniversary is a freight train car, which will be placed directly in front of the main gate. The train car is dedicated to the memory of the approximately 420,000 Hungarian Jews who were deported to Auschwitz.

The United Nations declared January 27 as the International Holocaust Memorial Day in 2005. Observed annually, it marks the liberation of Auschwitz in 1945 and remembers the six million Jews who lost their lives under theNazis.

Germany’s Scholz said in a Monday statement: “Sons, daughters, mothers, fathers, friends, neighbors, grandparents: more than one million individuals with dreams and hopes were murdered in Auschwitz by Germans. We mourn their deaths. And express our deepest sympathy. We‘ll never forget them. Not today, not tomorrow.”

The museum says the event at Auschwitz offers the chance for shared commemoration and global reflection.

It comes at a time of mounting antisemitism in Europe, fueled by conflict in the Middle East which saw Israel launch a war on Gaza in response to terror attacks carried out by Palestinian militant group Hamas on October 7, 2023.

There has been an increase in antisemitic incidents in Europe since October 2023, with some Jewish community organizations reporting an increase of more than 400%, according to a survey from the European Union Agency for Fundamental Rights (FRA), published in June.

Of those surveyed by the FRA, 76% say they hide their Jewish identity at least occasionally and 34% avoid Jewish events or sites due to feeling unsafe.

“Europe is witnessing a wave of antisemitism, partly driven by the conflict in the Middle East. This severely limits Jewish people’s ability to live in safety and with dignity,” FRA Director Sirpa Rautio said.

Events in the Middle East have also prompted a surge in Islamophobic incidents across Europe, including arson, verbal and physical abuse and the targeting of mosques.

NOT INTENDED FOR DISTRIBUTION TO UNITED STATES NEWS WIRE SERVICES OR FOR DISSEMINATION IN THE UNITED STATES

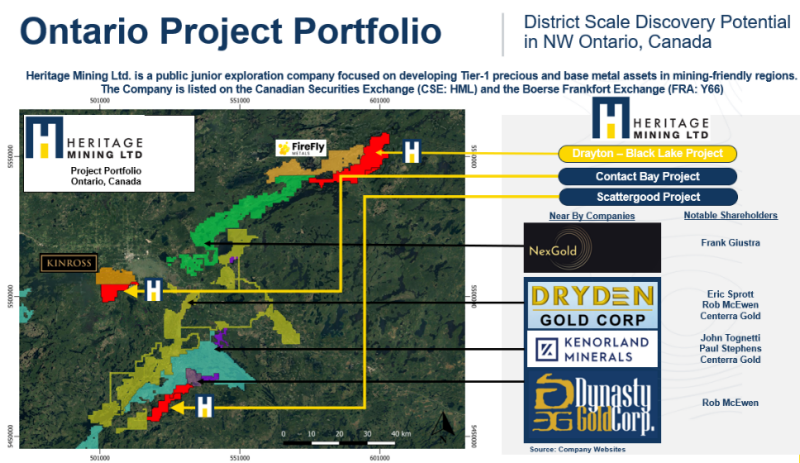

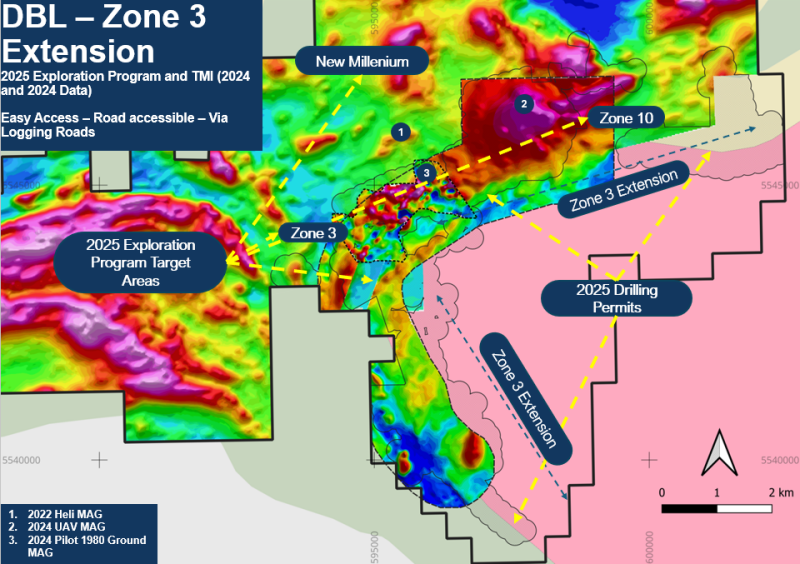

VANCOUVER, BC TheNewswire – January 27, 2025 Heritage Mining Ltd. (CSE: HML FRA:Y66) (‘ Heritage ‘ or the ‘ Company ‘) is pleased to announce it has exercised as received its drilling permits in respect to its Zone 3 Extension application (Figure 2) within its flagship Drayton Black Lake project (‘ DBL ‘) (Figure 1). The Company is also pleased to announce it has entered into an additional drill program contract, a labour contract and a Dozer D5 lease to support exploration activities at DBL. The Company’s drilling team is mobilizing as of January 26, 2025 with drilling set to commence February 10 th 2025.

Highlights:

Zone 3 Extension – +10km permit approval for Diamond Drilling (Figure 2)

Labour Contract – 2025 Diamond Drill Program Minimum 4,000m and D5 Dozer Lease

Diamond Drill Mobilization Date January 26, 2025, Drill Start Date February 10, 2025

Click Image To View Full Size

‘We are thrilled to have received our diamond drill exploration permit, we now are fully permitted for the Zone-3 Extension. This area was recently staked in relation to the identification of a new mineralization system, intrusive related gold. Furthermore, securing key contracts in respects to drilling and confirming drill start date is a key update to all Stakeholders. Target areas of interest include: DBL (New Millennium, Zone 3, Zone 3 Extension and Zone 10) and Contact Bay – Rognan Mine Area). We look forward to updating the marketplace in short order on progress.’ Commented Peter Schloo, President, CEO and Director of Heritage.

Click Image To View Full Size

Figure 2 – DBL – 2025 Exploration Program and Diamond Drill Permit Area

Qualified Person

Mitch Lavery P. Geo, Strategic Advisor for the Company, serves as a qualified person as defined by National Instrument 43-101 – Standards of Disclosure for Mineral Projects and has reviewed the scientific and technical information in this news release, approving the disclosure herein.

ABOUT HERITAGE MINING LTD.

The Company is a Canadian mineral exploration company advancing its two high grade gold-silver-copper projects in Northwestern Ontario. The Drayton-Black Lake and the Contact Bay projects are located near Sioux Lookout in the underexplored Eagle-Wabigoon-Manitou Greenstone Belt . Both projects benefit from a wealth of historic data, excellent site access and logistical support from the local community. The Company is well capitalized, with a tight capital structure.

For further information, please contact:

Heritage Mining Ltd.

Peter Schloo, CPA, CA, CFA

President, CEO and Director

Phone: (905) 505-0918

Email: peter@heritagemining.ca

FORWARD-LOOKING STATEMENTS

This news release contains certain statements that constitute forward looking information within the meaning of applicable securities laws. These statements relate to future events of the Company. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as ‘seek’, ‘anticipate’, ‘plan’, ‘continue’, ‘estimate’, ‘expect’, ‘forecast’, ‘may’, ‘will’, ‘project’, ‘predict’, ‘potential’, ‘targeting’, ‘intend’, ‘could’, ‘might’, ‘should’, ‘believe’, ‘outlook’ and similar expressions are not statements of historical fact and may be forward looking information. All statements, other than statements of historical fact, included herein are forward-looking statements.

Forward looking information involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance, or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by the forward-looking information. Such risks include, among others, the inherent risk of the mining industry; adverse economic and market developments; the risk that the Company will not be successful in completing additional acquisitions; risks relating to the estimation of mineral resources; the possibility that the Company’s estimated burn rate may be higher than anticipated; risks of unexpected cost increases; risks of labour shortages; risks relating to exploration and development activities; risks relating to future prices of mineral resources; risks related to work site accidents, risks related to geological uncertainties and variations; risks related to government and community support of the Company’s projects; risks related to global pandemics and other risks related to the mining industry. The Company believes that the expectations reflected in such forward-looking information are reasonable, but no assurance can be given that these expectations will prove to be correct and such forward‐looking information should not be unduly relied upon. These statements speak only as of the date of this news release. The Company does not intend, and does not assume any obligation, to update any forward‐looking information except as required by law.

This document does not constitute an offer to sell, or a solicitation of an offer to buy, securities of the Company in Canada, the United States, or any other jurisdiction. Any such offer to sell or solicitation of an offer to buy the securities described herein will be made only pursuant to subscription documentation between the Company and prospective purchasers. Any such offering will be made in reliance upon exemptions from the prospectus and registration requirements under applicable securities laws, pursuant to a subscription agreement to be entered into by the Company and prospective investors.

Copyright (c) 2025 TheNewswire – All rights reserved.

Cygnus Metals is focused on advancing its highly prospective copper-gold and lithium projects located in prolific mining regions in Quebec, Canada, boasting a high-grade copper and gold resource of 10.8 million tons @ 3.5 percent copper equivalent, and existing infrastructure that includes a 900 ktpa processing facility. The company is strategically positioned to become Quebec’s next copper producer.

Overview

Cygnus Metals (TSXV:CYG) is a copper-gold and lithium exploration and development company, positioning itself as a near-term producer in the prolific Chibougamau region of Québec, Canada. With a clear strategic focus, Cygnus Metals is actively advancing its assets toward production, taking advantage of its brownfields high-grade copper and gold projects, existing infrastructure, and supportive jurisdiction. The company’s overarching goal is to establish itself as Quebec’s next copper producer, with a hub-and-spoke mining strategy centered around its Copper Rand mill.

Following its strategic merger with Dore Copper, Cygnus Metals has consolidated a significant land package in prolific mining regions in Quebec – Chibougamau (copper-gold) and James Bay (lithium) – boasting a high-grade copper and gold resource of 10.8 million tons (Mt) @ 3.5 percent copper equivalent, and existing infrastructure that includes a 900 ktpa processing facility.

Cygnus Metals is currently focused on advancing the Chibougamau project, which is located within an area known for its historical copper and gold production, within the world-renowned Abitibi Greenstone Belt.

The company is unique because it owns the only mill in the area. The Copper Rand mill is designed to process an average of 1,350 tonnes-per-day and will need to be refurbished. This infrastructure gives Cygnus Metals a significant competitive advantage, both in terms of reducing capital expenditure requirements and potentially generating additional revenue streams by processing ore from third-party operations.

Québec, as a mining jurisdiction, provides strong support for mineral exploration and development. It ranks highly in the Fraser Institute’s rankings of mining-friendly jurisdictions, offering political stability, favorable tax incentives, and access to well-established infrastructure, including roads, rail, and power.

Cygnus Metals is led by an experienced and highly skilled management team. Ernest Mast, the company’s president and managing director, has over three decades of experience in the mining industry, including leadership roles at companies such as Primero Mining and Minera Panama (Inmet Mining). Mast’s background in managing junior and small-cap mining companies is well-suited to Cygnus Metals’ current development phase. The broader management and technical teams bring a wealth of operational expertise, with several individuals having extensive experience in exploration, project development, and mining operations in Canada and internationally.

Company Highlights

Cygnus Metals has consolidated a significant land package within the prolific mining regions of Quebec, Canada: Chibougamau and James Bay.

The 100 percent owned Copper Rand mill will be refurbished for future production and will be the only operating mill in the Chibougamau region. The mill will have extra capacity and provides the ability to process its own ore while potentially offering toll milling services to other nearby mining projects.

Cygnus Metals is led by an experienced and highly skilled management team.

Key Project

Location of the Chibougamau Project relative to other major deposits and processing facilities

Cygnus Metals’ assets are located within two well-known mining regions in Quebec, with a long history of production. The company’s current strategy revolves around a hub-and-spoke model, with the Copper Rand mill serving as the processing hub, fed by multiple satellite deposits.

Chibougamau Copper Gold Project

Located within a historic, high-grade mining camp, the Chibougamau copper gold project spans 187 sq km and includes a 900 ktpa processing plant and existing major infrastructure. The project consists of seven exploration targets, three of which have an existing mineral resource 10.8 million tons @ 3.5 percent copper equivalent.

The Chibougamau region has a rich mining history dating back to the early 1900s. With 16 historic mines, the district has produced some 53.5 Mt @ 3.4 percent copper equivalent (1.8 percent copper and 2.1 grams per ton gold) for 945,000 of copper and 3.5 Moz of gold.

The PEA for the project anticipates a mine life of over 10 years, with the potential to produce 53 million pounds of copper equivalent annually. Metallurgical testing at Corner Bay has yielded positive results, with copper recoveries ranging from 96.8 percent to 98.2 percent, and the concentrate is of high commercial quality, making it highly attractive to smelters.

Cygnus is focused on growing the mineral resources base at the Chibougamau project and move towards a feasibility study. The resource base, which currently stands at 3.6 Mt of measured and indicated mineral resources at 3 percent copper equivalent and 7.2 Mt of inferred mineral resources at 3.8 percent copper equivalent, for a total of 10.8 Mt at 3.5 percent copper equivalent for 306 kt copper and 314 koz gold. The project includes three key assets with existing– Corner Bay, Devlin, Cedar Bay and Joe Mann – all located within 50 km of the central 900 ktpa processing facility.

The Corner Bay deposit is the cornerstone of the project, demonstrating exceptional grades and exploration potential, positioning it as one of the highest-grade copper projects in North America. The latest resource estimate, as of 2022, includes 2.7 million tonnes of indicated resources at a grade of 2.66 percent copper and 5.8 million tonnes of inferred resources at a grade of 3.44 percent copper. The deposit remains open in several directions and at depth, suggesting that further drilling could potentially expand the resource base and extend the mine life.

Newly staked ground over the highly prospective Chibougamau Pluton and surrounding anorthositic host rock

Devlin is a smaller satellite deposit located approximately 10 kilometers west of Corner Bay. The project has a measured and indicated resource of 775,000 tonnes at a grade of 2.17 percent copper, along with an inferred resource of 484,000 tonnes at a grade of 1.79 percent copper. While Devlin’s size is modest compared to Corner Bay, it plays a crucial role in Cygnus Metals’ hub-and-spoke mining strategy. Ore from Devlin will be transported to Corner Bay for pre-concentration, before being trucked to the Copper Rand mill for final processing. The company is planning to employ room-and-pillar and drift-and-fill mining methods at Devlin, with operations expected to commence shortly after Corner Bay comes online.

Cedar Bay is a past-producing mine located near the Copper Rand mill. It produced 3.9 million tons of ore at an average grade of 1.63 percent copper and 3.21 grams per ton gold during its operating life. Drilling programs have defined in the southwest zone 130,000 tons of indicated resources at a grade of 9.44 grams per ton gold and 1.55 percent copper, and 230,000 tons of inferred resources at a grade of 8.32 grams per ton gold and 2,13 percent copper.

The Joe Mann gold-copper deposit is another component of Cygnus Metals’ hub-and-spoke strategy. Located 60 km south of the Copper Rand mill, Joe Mann produced 1.2 million ounces of gold and 28 million pounds of copper over its mine life, at an average grade of 8.26 grams per ton gold and 0.25 percent copper. The current resource estimate includes 608,000 tons of inferred resources, with an average grade of 6.78 grams per ton gold and 0.24 percent copper.

Board and Management

David Southam – Executive Chairman

David Southam is highly experienced in operations, project development and capital markets across the resources and industrial sectors. He was previously the managing director of Mincor Resources. Southam is non-executive director of Ramelius Resources and non-exec chair of Andean Silver Limited.

Ernest Mast – President and Managing Director

Ernest Mast has 30 years of experience in various technical and executive roles in the mining industry, across a wide range of commodities, geographies and development stages. Mast is on the board of Scottie Resources. Mast previously held the positions of president and chief executive officer at Primero Mining, vice president of corporate development at Copper Mountain Mining, vice president of operations at New Gold and president and CEO of Minera Panama S.A., Inmet Mining Corporation’s subsidiary, developing the $6 billion Cobre Panama project. Mast began his career with Noranda and its affiliates, where he took on roles of increasing responsibility over a 20-year timeframe. Mast is a member of l’Ordre des ingénieurs du Québec and has a bachelors’ and masters’ degree in metallurgical engineering from McGill University. Mast also received post-secondary business training at Henley College in the UK and at the Universidad Catolica in Chile.

Mario Stifano – Non-executive Director

Mario Stifano is a seasoned mining executive and chartered professional accountant with over 16 years of experience working with exploration, development and producing mining companies. Stifano is currently the chief executive officer of Galantas Gold. Stifano has held a number of senior executive positions including chief executive officer of Cordoba Minerals, executive chairman with Mega Precious Metals, vice president and chief financial officer with Lake Shore Gold, and vice president and chief financial officer of Ivernia. Stifano has been instrumental in raising over $700 million to explore and fund mining projects, including raising over $500 million at Lake Shore Gold, to develop three gold mines which are currently producing over 180,000 ounces of gold annually, and are now part of the Canadian assets within Pan American Silver.

Kevin Tomlinson – Non-executive Director

Kevin Tomlinson is a structural geologist and investment banker. He is the non-executive chair of Bellevue Gold and of FireFly Metals. Tomlinson has a successful track record in base and precious metals project development.

Raymond Shorrocks – Non-executive Director

Raymond Shorrocks brings a wealth of experience in corporate finance, stockbroking and financial services in Ontario. He was the previous non-executive chair of FireFly Metals and Bellevue Gold. He is the executive chair of Alicanto Minerals.

Brent Omland – Non-executive Director

Brent Omland is the co-CEO of Ocean Partners providing a range of trading services for miners, smelters and refiners globally. He is a chartered accountant and has held CFO roles for publicly listed companies in the resources industry.

When the Trump administration announced a return-to-office mandate this week, it stated Americans “deserve the highest-quality service from people who love our country.”

Federal employees like Frank Paulsen say that comment suggests they aren’t hardworking or loyal.

Paulsen, 50, is the vice president of the Local 1641 chapter of the National Federation of Federal Employees, a federal workers union. He works as a nurse at the Department of Veterans Affairs in Spokane, Washington, and has been teleworking three days a week since 2022. His main job involves processing referrals to send patients to community health care partners, something he can do remotely.

Paulsen said he has been a federal employee for 22 years and is a disabled veteran himself. And he doesn’t think anyone he works with isn’t measuring up.

“I do not believe that I would subscribe to that belief at all,” Paulsen said. “My co-workers are very diligent about getting the work done.”

On Monday, Trump signed an executive order mandating all federal agencies order their employees back into the office full time “as soon as practicable” alongside a directive to end remote-work arrangements except as deemed necessary.

Late Wednesday, administration officials released a more detailed directive demanding the termination of all remote-work arrangements, alongside a statement that it’s a “glaring roadblock” to increasing government performance that most federal offices are “virtually abandoned.”

The GOP has long bemoaned the state of the federal bureaucracy. But the Trump administration appears to be making good on promises to overhaul it, in part supported by Elon Musk, Trump’s biggest donor, who is now serving as a semiofficial adviser.

“This is about fairness: it’s not fair that most people have to come to work to build products or provide services while Federal Government employees get to stay home,” Musk wrote on X following the order’s signing.

Though it represents just a sliver of the nation’s overall workforce, the U.S. government is the country’s largest employer, with more than 2 million civilian employees. Some 162,000 workers alone are located in Washington, D.C., according to data from the Office of Personnel Management (OPM), and federal workers make up over 40% of the city’s workforce.

But most federal workers, like Paulsen, actually work in other parts of the country: Only 7.56% of federal employees work in D.C.

Yet whatever their location, many workers like Paulsen are responding to Trump’s RTO order with concern. There are practical worries: Paulsen has questioned whether the office he works in, which the VA leases, has enough seats for everyone employed by his division. Another VA employee, who requested anonymity because she didn’t want her program targeted, echoed space concerns, especially in settings where sensitive medical information is discussed.

Paulsen said he is planning for a return to the office five days a week no matter what.

“The guidance we give our employees is basically, don’t put yourself in a position to get fired,” he said.

Morale has never been lower on one metastatic cancer research team within the VA, an employee there told NBC News. She requested her name not be used because she didn’t want her team to lose funding. Two people on her team are remote workers and the employee said she works from home two days a week, doing administrative tasks and data analysis.

Guidance was changing by the hour on Thursday, she said. With a contract that renews every three years, the employee said she was told by management at one point to start looking for new jobs, then was later alerted by a higher-up that she fell into the VA’s list of exemptions.

Lunch hour at a restaurant in the Capitol Hill neighborhood of Washington, D.C., in 2021.Drew Angerer / Getty Images file

The fate of her remote colleagues and telework options remains unclear, she said. They work with veterans across the country, and the team worried for those whose treatments could be canceled without them.

“It just doesn’t feel good to go into work knowing that you don’t know if you’re going to have a job in a few months,” she said.

A U.S. Department of Agriculture employee who works in Washington, D.C., said he and his colleagues are making backup plans. They all have telework arrangements, and some work remotely — hourslong drives from the nearest federal office. He views the executive order as an attempt to force people to quit. He wanted to remain anonymous because he fears retaliation.

“The feeling is there’s an ax over our heads,” he said.

The Trump administration has said that just 6% of federal employees now work in person. But according to an August report from the Office of Management and Budget, among federal workers eligible for telework — and excluding those who are fully remote — roughly 61% of work hours are now in person.

Among agencies, the Department of Agriculture had the highest percentage of in-person work hours, at 81%; while the Environmental Protection Agency had the lowest, at about 36%.

The Biden administration had already been keeping an eye on return-to-office implementation as the Covid-19 pandemic waned, with regular reports being issued on how much telework was being used by each federal agency.

In December, an OPM survey found 75% of telework-eligible employees had participated in telework in fiscal year 2023, though that was 12 percentage points lower than in fiscal year 2022.

The report said there had been positive results from a hybrid setup.

“Agencies report notable improvements in recruitment and retention, enhanced employee performance and organizational productivity, and considerable cost savings when utilizing telework as an element of their hybrid work environments,” it said.

A GOP-sponsored House Oversight Committee report this week accused the Biden administration of exaggerating in-office attendance, citing “physical and anecdotal evidence,” while accusing it of taking a “pliant” posture toward federal union groups as they sought more generous telework arrangements.

Even as it praised Trump’s desire to improve federal workforce accountability and performance, the Partnership for Public Service, a nonpartisan think tank focused on government effectiveness, said in a statement that the return-to-office order was an example of overreach.

‘While any move toward making the government more responsive to the public should be welcomed, it said, the actions announced in Trump’s workforce-related executive orders put that goal “farther out of reach.”

On a press call with reporters this week, Partnership CEO Max Stier saidtelework is necessary to attract more qualified employees who already tend to enjoy higher salaries in the private sector.

In a follow-up statement, Stier warned of the dramatic impact the order will have on career civil servants’ personal lives.

“The affected employees are everyday people who have to support themselves and their families, and the abrupt and rushed approach chosen here will have a traumatizing impact on not just them but their colleagues who remain in their roles serving the public, as well,” Stier said.

Social media forums frequented by government workers have also lit up, with many raising questions about how agencies were expected to comply given that many have been downsizing their office space.

Even before the pandemic ushered in widespread work-from-home policies, 2010 legislation cited telework for federal employees as a way to reduce office costs and promote resilience in emergency situations, as long as employees continued to meet performance expectations.

The Wall Street Journal reported the government was looking to sell off many of its commercial real estate holdings. NBC News could not independently confirm the report.

Unions representing federal employees have slammed the new policy, saying it would undermine the government’s effectiveness and make it harder for agencies to recruit top talent.

“Rather than undoing decades of progress in workplace policies that have benefited both employees and their employers, I encourage the Trump administration to rethink its approach and focus on what it can do to make government programs work better for the American people,” Everett Kelley, the president of the American Federation of Government Employees, said in a statement.

The AFGE’s contracts with major government firms, including the Environmental Protection Agency and the Department of Education, establish procedures for telework and remote work in accordance with the 2010 law. The union said the order “doesn’t appear to violate any collective bargaining agreements,” and whether it would file a lawsuit depends on how the policy is implemented.

“If they violate our contracts, we will take appropriate action to uphold our rights,” the AFGE said in a statement.

The NFFE, Paulsen’s union, likewise said the executive orders would “impair critical services” and viewed the termination of remote work arrangements as an attempt to force employees to quit.

“I am worried about this administration violating those contracts with regard to telework,” Randy Erwin, the national president of the NFFE, told NBC News.

One sector that would stand to benefit from the mandate is local business in downtown Washington, D.C.

Gerren Price, the president of the DowntownDC Business Improvement District, which covers an area to the east of the White House, said only about half of the office space within its boundaries is occupied. Price said 27% of that office space is owned and operated by the federal government.

From coffee shops to dry cleaners, local businesses that used to cater to a nine-to-five crowd have closed, Price said.

Leona Agouridis, the president of the Golden Triangle Business Improvement District, which encompasses an area between the White House and Dupont Circle a mile to the north, said the neighborhood hasn’t felt as busy as it did before the pandemic.

“This will go a long way in bringing back vibrancy that we have lost over the last five years,” Agouridis said.

At the Tune Inn, a restaurant and bar that has served D.C.’s Capitol Hill neighborhood since 1947, general manager Stephanie Hulbert is bringing back a federal worker lunch discount, which the establishment had done away with after the pandemic because no one used it. She knows this policy will change many federal workers’ lives, but hopes they can help each other out.

“I really hope that when these workers do come back, they come and support the small businesses that need it in D.C.,” Hulbert said. “Hopefully we’ll be able to get the morale up to where it needs to be.”